Under the African Continental Free Trade Agreement over 1.3 billion people will be connected into a single market.

The continent’s automotive industry is set to benefit from this trend, as 54 countries are accelerating their integration into a single, tariff-free market.

According to a new report by the World Economic Forum – AfCFTA: A New Era for Global Business and Investment in Africa – global business will play a key role in boosting the industry by $12 billion by 2027 under the AfCFTA.

Transformative change is underway in the African automotive industry as trade begins under the African Continental Free Trade Area (AfCFTA).

The continent’s auto industry, valued at $30 billion in 2021, is expected to grow to $42 billion by 2027 — a nearly 40% increase in value.

Much of this growth can be serviced by local companies within the newly established free trade area. Under the AfCFTA, over 1.3 billion people will be connected into a single market. For the automotive industry, that’s a significant opportunity.

Building on a successful automotive industry through AfCFTA

International companies have found success in the automotive industry by partnering with African countries, signalling that the automotive sector is ripe for new and increased investment strengthened by the AfCFTA.

Across the continent, there is an average annual demand for 2.4 million motor cars and 300,000 commercial vehicles. This domestic demand — which is rising due to the continent-wide increase in disposable income, strong growth of the middle class and rapid urbanisation — is currently being met primarily by imported used vehicles.

However, domestic production has also been growing by an average of 7% annually over the past few years. Today, Morocco and South Africa are leading the way as major players in the automotive sector, making up 80% of African exports, with Algeria also experiencing rapid growth.

An African economy of scale

The AfCFTA unlocks several opportunities for African and global businesses in the automotive industry to seize, building upon strong foundations in a new era of frictionless African trade.

African automotive manufacturers will benefit from all the advantages of economies of scale; essential for the competitive manufacturing of automotives. Reduced tariffs across the continent for inputs like aluminium from Mozambique or rubber in Cote d’Ivoire will mean the African industry as a whole becomes more dynamic. The AfCFTA’s rules of origin will also help set common thresholds for value-added levels, and if these are progressively harmonised across regional communities, these more general and co-equal rules will help stimulate trade.

The continent’s leadership is actively working towards improving the investment environment for the automotive sector specifically. There is significant political will by African governments and private sector players to develop automotive regional value chains because of the sector’s historic contribution to industrialisation.

Afreximbank, for example, and the African Association of Automotive Manufacturers are working together to support the industry by helping harmonise automotive standards, developing a focused training programme for the public and private sectors and providing financing to industry players across the value chain, with Afreximbank committing $1 billion to the industry through direct financing and partnerships.

Sustainability and the global fight against climate change also stand to benefit from the new trade area. Africa could be a key region for promoting sustainable mobility by harnessing renewable energy as demand for electric vehicles and motor vehicles grows.

Electric vehicles currently make up less than 1% of sales in South Africa, but demand is growing across the continent as some of Africa’s main trading partners have banned internal combustion engine vehicle sales, effective as early as 2035. Already, there are pilot projects for sustainable vehicles in Rwanda, Egypt and South Africa, and e-mobility startups have emerged across the continent.

Africa has a great wealth of the natural resources that are key raw materials for modern vehicles, and several countries have their own procurement markets for materials such as copper, platinum, cobalt, bauxite and lithium — essential materials for the suite of new technologies required to reach net-zero. There is also a huge market for motorcycles in Africa — especially in west, east and north Africa — as well as electric two-wheelers, meaning more opportunities for using domestically produced inputs in new markets by leveraging AfCFTA preferences.

Case study: Volkswagen’s success

German auto giant Volkswagen, already a key player on the continent, has recognised the potential of the AfCFTA to catalyse local production of automotives and meet local demand. To date, the company has successfully established local assembly operations in Kenya, Rwanda and Ghana as well as two wholly owned subsidiaries in Rwanda and Ghana.

The company attributes its success in Africa thus far to its collaboration with African governments in developing and implementing automotive policies in their respective countries, including South Africa, Morocco, Tunisia, Ghana, Egypt and Kenya. Volkswagen recognises that the increase in local manufacturing requires different levels of investment and depends on consistent, enabling industrial policies with access to local markets — which it sees as a major benefit of the AfCFTA.

The key industry trends reviewed here and the opportunities opening up as a result of the AfCFTA, coupled with Volkswagen’s experience of success, provide a powerful case for new investors to move into the automotive sector and thus help drive and transform economies across the continent.

This article first appeared here.

*****

De-Dollarization: More Countries Seek Alternatives to the US Dollar

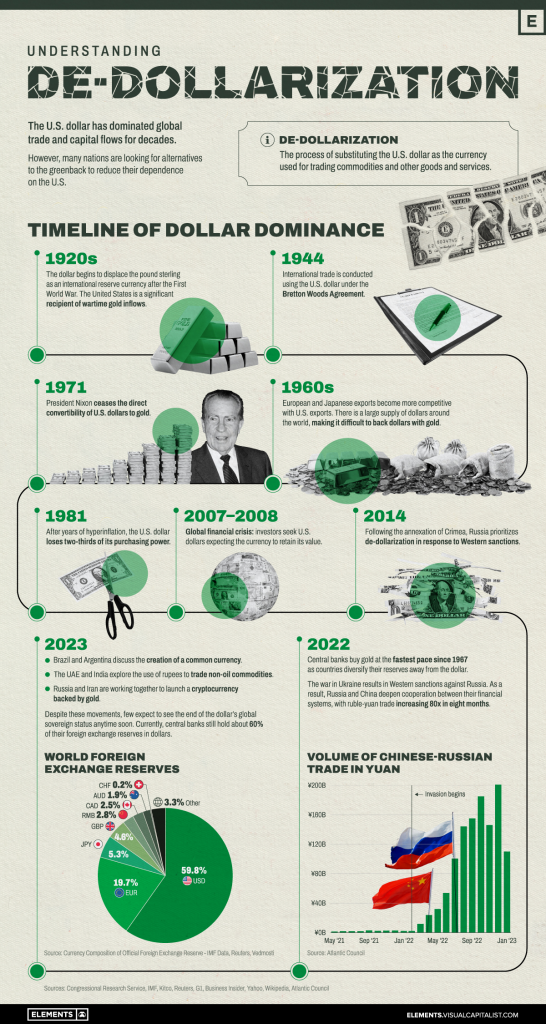

The US dollar has dominated global trade and capital flows for many decades.

However, many nations are looking for alternatives to the greenback to reduce their dependence on the United States.

These graphic below catalogues the rise of the dollar as the dominant international reserve currency, and the recent efforts by various nations to de-dollarize and reduce their dependence on the US financial system.Dollar Dominance

The US became, almost overnight, the leading financial power after World War I.

The country entered the war only in 1917 and emerged far stronger than its European counterparts.

As a result, the dollar began to displace the pound sterling as the international reserve currency and the US became a significant recipient of wartime gold inflows.

The dollar then gained a greater role in 1944, when 44 countries signed the Bretton Woods Agreement, creating a collective international currency exchange regime pegged to the US dollar which was, in turn, pegged to the price of gold.

By the late 1960s, European and Japanese exports became more competitive with US exports.

There was a large supply of dollars around the world, making it difficult to back dollars with gold.

President Nixon ceased the direct convertibility of US dollars to gold in 1971.

This ended both the gold standard and the limit on the amount of currency that could be printed.

Although it has remained the international reserve currency, the US dollar has increasingly lost its purchasing power since then.

Russia and China’s Steps Towards De-Dollarization

Concerned about America’s dominance over the global financial system and the country’s ability to ‘weaponize’ it, other nations have been testing alternatives to reduce the dollar’s hegemony.

As the US and other Western nations imposed economic sanctions against Russia in response to its invasion of Ukraine, Moscow and the Chinese government have been teaming up to reduce reliance on the dollar and to establish cooperation between their financial systems.

Since the invasion in 2022, the ruble-yuan trade has increased eighty-fold.

In addition, central banks (especially Russia’s and China’s) have bought gold at the fastest pace since 1967 as countries move to diversify their reserves away from the dollar.

How Other Countries are Reducing Dollar Dependence

In recent months, Brazil and Argentina have discussed the creation of a common currency for the two largest economies in South America.

In a conference in Singapore in January, multiple former Southeast Asian officials spoke about de-dollarization efforts underway.

The UAE and India are in talks to use rupees to trade non-oil commodities in a shift away from the dollar.

For the first time in 48 years, Saudi Arabiasaid that the oil-rich nation is open to trading in currencies besides the US dollar.

Despite these movements, few expect to see the end of the dollar’s global sovereign status anytime soon.

Currently, central banks still hold about 60% of their foreign exchange reserves in dollars.

****

How technology will transform African business?

Technology will transform the way the Africa conducts business and there is great excitement about developments in the digitalisation space.

However, it is imperative that the regulatory banking environment keeps pace with technology and does not hinder innovation.

Never has debate about digitalisation and automation been so fierce, and its interaction with fintech solution providers in the trade finance space.

This is transformative for the way the continent conducts business.

Such discussions no longer centre on the exciting technologies that are out there, but about how they can help solve specific problems and future-proof businesses.

Several digitalisation trends exist today, which can broadly be divided into a few main areas:

· Data to make better decisions;

· Technology that drives efficiencies;

· Risk management and mitigation tools; and

· Viewed holistically, solutions that will allow us to future-proof trade businesses.

One example is optical correction recognition (OCR). When importing or exporting goods, be aware of the amount of paperwork that is generated and the time it takes to assess this paperwork at various points in the process.

OCR technology has allowed not only to streamline and build more resilience in trade processes, but to process more documents under letters of credit than a bank would have been able to manually.

This frees us up valuable time.

Taking this a step further, Africa is becoming increasingly important in the global economy, from both an import and export perspective.

While Africa has enjoyed long-standing relationships with the EU and US, some of its biggest growth markets are in the Asian economies and as access-to-market opportunities increase, so will the demand for trade finance.

However, to take advantage of such opportunities, it’s important that the banking regulatory framework keeps pace with the new technology.

There is always a natural tension between the regulatory requirements faced by the banking sector and the flexibility enjoyed by many of the fintech disrupters.

On one hand, Africa has an annual trade finance gap of about $100bn each year.

On the other, the banking sector is busy rolling out Basel IV regulations.

Given the more stringent capital requirements of these regulations, unless something drastically changes, they may restrict the ability of banks to lend to small and medium-sized businesses.

One of the main concerns with Basel IV regulations is the effective tenor of trade finance transactions.

Trade finance is short-term in nature, and capital regulations should be based on three- to six-month maturity profiles instead of insisting on any tenor that is one year or above.

Such regulations mean that it may cost lenders more to be innovative.

Instead, businesses and financial institutions should be rewarded for unlocking financing that empowers youth and women-owned small businesses.

Africa is going through a unique period of economic growth as it starts to adjust to a changing world order and the associated economic events.

Events in Ukraine, Russia and China have materially disrupted global supply chains, and this is forcing Africa to fast-track many of its infrastructure projects.

With the narrowing of both the infrastructure and trade finance gaps, Africa has the chance to lean on technology to help unlock trade funding to empower the next generation of entrepreneurs on the continent.

======

This is a summary from an article published by Absa CIB’s Head of Trade Finance, Bohani Hlungwane, which first appeared here.

****

The European Parliament approved legislation to phase in a levy on high-carbon imports based on the CO2 emitted in producing them.

This law is a world-first and awaits final approval from EU countries – expected within a few weeks.

The tax aims to put pressure on countries outside of EU borders to put a price on CO2 emissions – while also countering the benefits to EU industries relocating to regions with weaker environmental laws.

The tax gives credit to countries that put a price on carbon, allowing importers of goods from those countries to deduct payments made for overseas emissions from the amount owed at the EU’s borders.

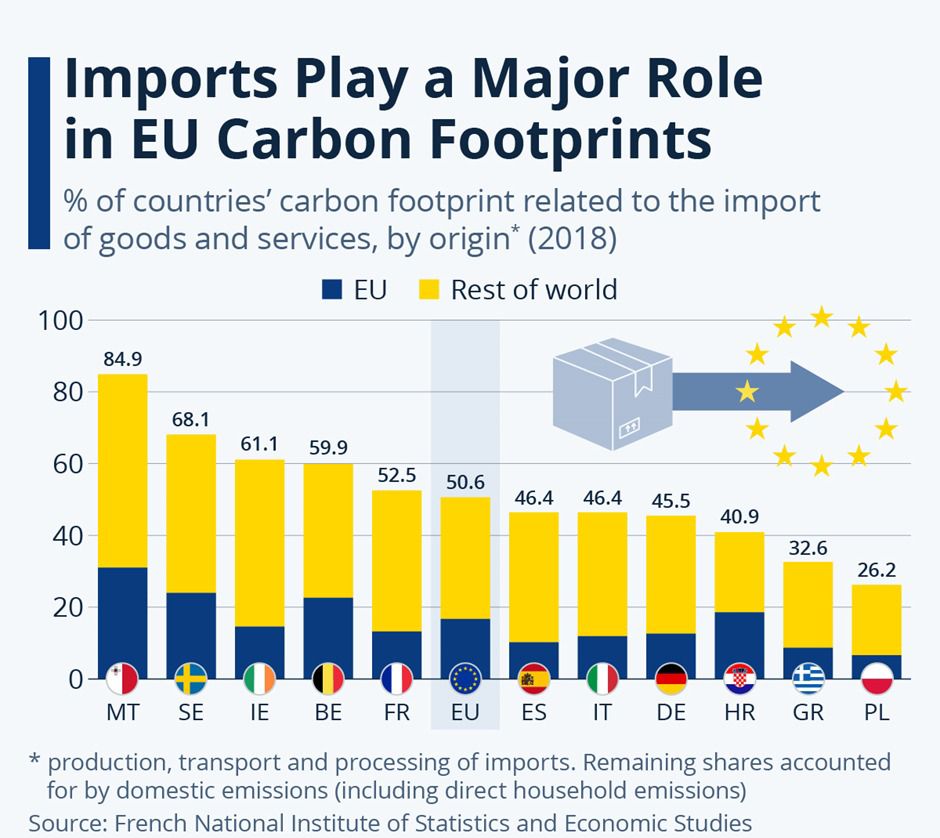

If we take into account the size of the population, China emits 2 times more carbon dioxide per capita than the world average, the EU 1.5 times more and the United States 3 times more.

But these figures do not account for emissions associated with imported goods and services, for which much of the production (and carbon footprint) is located in manufacturing countries that still rely heavily on fossil fuels.

When including the impact of products that are used locally but manufactured abroad, the carbon footprint per capita in the EU is higher than in China: 11 tons of CO2 equivalent per year compared to 8. The figure for the United States is 21 tons.