*** David Mosaka, Chief Ratings Officer at the Sovereign Africa Ratings (SAR) ***

By David Mosaka

This is an unsolicited credit rating review of South Africa by the Sovereign Africa Ratings (SAR) which also confirms that the credit rating has been disclosed to the rated entity…

RATING ACTION

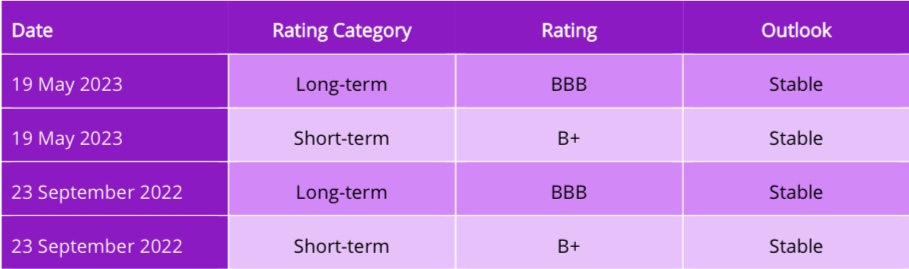

Sovereign Africa Ratings (SAR) has affirmed South Africa’s long-term and short-term credit ratings at BBB and B+ respectively, with a Stable outlook. These ratings and outlook reflect SAR’s expectation of solid financial, fiscal, and monetary flexibility despite the economic challenges faced by the country in the near to medium term. One of the main challenges is the electricity shortage, which is expected to reduce the Gross Domestic Product (GDP) by 2%, resulting in an estimated growth of only 0.3%. Other obstacles to growth include inflation, increasing interest rates, global economic slowdown, geopolitical tensions, lack of consumer and business confidence, the high unemployment rate of 32%, and inefficiencies in state- owned enterprises. These factors present credit challenges.

KEY FACTORS INFLUENCING THE RATINGS

South Africa’s economy is gradually becoming more resilient to electricity shortages as alternative sources of energy become more accessible and affordable. Private sector investment in the energy sector has increased, especially following the introduction of the President’s ‘Energy Action Plan.’ If effectively implemented, this plan should enhance energy security and contribute to economic revitalisation in the coming years.

The government’s focus on infrastructure development, including increased involvement of the private sector, is expected to lead to announcements regarding ports, transport, and water projects in 2023 and ongoing work in 2024. Global inflationary pressures are projected to ease in the latter part of 2023, leading to interest rate cuts and improved global economic prospects starting in 2024.

Despite the challenging environment, there are growing investment opportunities in the infrastructure sector, particularly in energy generation, transmission, transport, logistics, water, and telecommunications. Policy and regulatory changes in these sectors have created space for increased private sector participation.

South Africa’s economy also possesses positive attributes, including a substantial external asset position, low levels of foreign currency debt, a large and diversified economy, export diversification, a robust financial system, and an effective exchange rate regime. The proactive monetary policy of the South African Reserve Bank, which has effectively managed inflation expectations, is also a positive factor contributing to the country’s credit strength.

Fiscal and structural challenges need urgent attention in conjunction with monetary policy measures.

Global Economic Environment

The global economy is expected to experience a significant slowdown in the current year, with the International Monetary Fund (IMF) projecting real output growth of 2.9%, down from the upwardly revised 3.4% in 2022. This forecast, released in the IMF’s World Economic Outlook Update in January, is a slight improvement from the IMF’s October forecast of 2.7% and is mainly attributed to the reopening of the Chinese economy.

Government Debt

South Africa’s gross debt is projected to rise from R4.73 trillion in 2022/23 to R5.84 trillion in 2025/26. However, it is expected to stabilise at 73.6% of GDP in 2025/26, compared to the Medium-Term Budget Policy Statement (MTBPS) projection of 71.4% in 2022/23. Thereafter, debt as a share of GDP is anticipated to decline. Contingent liabilities are also expected to decrease from R1.07 trillion in 2022/23 to R904.1 billion in 2025/26. This debt reduction and contingent liabilities positively affect fiscal flexibility and reduce the burden of debt.

South Africa’s external debt stands at 39% of GDP as of Q4 2022, with half of it denominated in foreign currency. Approximately 80% of external debt is long-term. Total external debt decreased from US$169.3 billion in June 2022 to US$157.

Total external debt decreased from US$169.3 billion in June 2022 to US$157.6 billion in September 2022, primarily due to a decrease in short-term debt. The decrease in external debt indicates improved external stability and reduced vulnerability to currency fluctuations.

Monetary Policy

The persistent issue of high inflation remains a major concern in 2023, as central banks approach the endgame of interest rate hikes. In the first quarter of 2023, consumer inflation in South Africa exceeded the target band, standing at 7.1%, which is 1.1 percentage points above the target. Despite interest rates reaching an all-time high recently, the South African Reserve Bank (SARB) will likely continue to raise rates to curb inflation. In March 2023, the SARB implemented its ninth consecutive interest rate hike as part of its unwavering commitment to combat inflation. The Central Bank’s monetary policy aims to keep inflation expectations anchored, which is considered a positive trend.

Monetary Policy Implementation Framework (MPIF)

Reforms in the MPIF are a positive step towards improving liquidity flows and maintaining financial stability in the monetary sector, particularly during times of crisis such as market disruptions. The reform ensures a transition to a modern system in the money market that relies on a consistent surplus of liquidity. This measure helps reduce liquidity risk in the South African banking sector.

Subdued Economic Growth

The South African Reserve Bank has revised its growth forecast downward for 2023 due to increased electricity disruptions and logistical constraints. As a result, the Central Bank now predicts a GDP growth rate of only 0.3%. This will have a short-term negative impact on national income and tax revenues.

Government Revenue

The proportion of government revenue as a percentage of GDP has shown volatility in recent years, reaching a peak during the 2018/19 financial year, followed by a significant decline in 2020 due to the financial crisis caused by the COVID-19 pandemic. Projections indicate that it will stabilise at 28% between 2023 and 2025. The projected gross tax revenue for the fiscal year 2022/23 is expected to amount to R1.69 trillion, which is R93.7 billion higher than the estimate in the 2022 Budget, indicating an upward revision of R10.3 billion from the estimate in the 2022 Medium-Term Budget Policy Statement (MTBPS). Furthermore, the tax-to-GDP ratio, which experienced a dip due to the financial crisis caused by COVID- 19, is expected to recover and reach 25.4% in the fiscal year 2022/23. This development is considered credit positive by the Sovereign Africa Ratings (SAR).

Government Expenditure

Consolidated government expenditure is projected to reach 32.6% of GDP in the fiscal year 2022/23 before decreasing to 31.2% in the fiscal year 2025/26. The 2023 Budget proposes a total consolidated government expenditure of R2.24 trillion for the fiscal year 2023/24, with a significant portion allocated to socio-economic programmes focusing on learning and culture (R457 billion), social development (R378 billion) (including funding for the COVID-19 social relief of distress grant until 31 March 2024), and health (R259 billion). Debt service costs remain one of the largest spending categories, amounting to R340 billion for the fiscal year 2023/24. Consolidated government spending is expected to increase to R2.47 trillion in the fiscal year 2025/26.

Public Sector Wage Bill

The public sector wage bill has experienced an average annual growth rate of 7.3% from the fiscal year 2014/15 to fiscal year 2019/20. However, it is projected to increase by an average of 3.3% over the medium term. If public sector wage increases exceed the range of 3% to 6% inflation, it will place a burden on the government’s finances and hinder efforts to achieve austerity measures. This could have a negative impact on the overall fiscal outlook.

Fiscal Balance

The fiscal balance is projected to further improve over the medium term, with a primary surplus expected in the fiscal year 2022/23 – the first since 2008/09. The 2023 Budget Review proposes debt relief of R254 billion over the next three years for Eskom to enhance its balance sheet and enable funding availability for maintenance. The scale of the debt relief increases government borrowing to the extent that gross loan debt now stabilises at a later time than originally projected, reaching 73.6% of GDP in the fiscal year 2025/26.

Rand Exchange Rate

The value of the rand has been negatively affected by electricity load-shedding. Additionally, the reduced outlook for domestic economic growth has influenced investor sentiment.

Logistics and Infrastructure Networks

Inadequate management, insufficient investment, and economic sabotage (theft) have turned South Africa’s logistics and rail infrastructure into a nationwide crisis. As a result, the country faces an annual opportunity cost of 2% of GDP. Fewer goods are being exported, and South African ports are losing their competitive advantage to other ports in the region, which negatively affects revenue earnings and results in missed opportunities.

The Sovereign Africa Ratings (SAR) has observed a positive development with the launch of the National Rail Policy (NRP). This policy aims to implement significant structural reforms in the rail freight industry. By allowing third parties to access the freight rail network, the policy seeks to revitalise the South African rail industry. The introduction of third-party access to the rail network in South Africa will not only breathe new life into the rail sector but also have a ripple effect in terms of attracting investment, creating jobs, and fostering economic growth. Increased freight transported by rail will necessitate additional capacity, which, in turn, will create more opportunities for local manufacturing.

Opening up the South African rail network to public-private partnerships also serves as a gateway for local goods to access the African market through the African Continental Free Trade Area.

ESG Imperatives

Environmental, Social, and Governance (ESG) imperatives have gained significant traction in South Africa and are now integral to the decision-making process for businesses. The country’s strong ESG credentials are essential for attracting additional capital inflows, which is a positive development for the South African economy. State-owned enterprises, including Eskom and Transnet, have been urged to adhere to the governance aspects of ESG imperatives, particularly in terms of their financial reporting compliance with International Financial Reporting Standards (IFRS) and the Public Finance Management Act (PFMA).

Socio-Economic Challenges: The World Economic Forum (WEF) highlighted various crises faced by global economies in 2023, including energy and the cost of living, fragmentation of the global economy, climate change, and the need for mitigation and adaptation. The National Treasury’s 2023 Budget Review allocated R695 million for immediate relief following recent floods and national disasters in various provinces, with an additional R1.0 billion allocated for fiscal year 2024/25. South Africa, like many other countries, faces social cohesion challenges due to the affordability issues associated with the cost-of- living crisis. Urgent action is required to address the obstacles of economic growth, unemployment, poverty, and inequality, as these factors have a negative impact on stimulating consumption expenditure, a key driver of economic growth.

Unemployment: Global economic slowdown, rising interest rates, and inflation are expected to weigh on employment prospects worldwide in 2023. Unemployment in South Africa is anticipated to be driven by factors such as economic deceleration, automation, and structural shifts in the labour market. The elevated levels of unemployment in the country have a detrimental effect on the tax revenue base, leading to a decline in individual income tax, which constitutes 37% of the total government revenue. Job creation efforts may face constraints due to the increased frequency and severity of electricity load- shedding, which adversely affects small and medium-sized businesses and adds to cost pressures over the medium term.

The African Continental Free Trade Area (AfCFTA)

The AfCFTA is a positive development that promotes beneficiation, inter-trade, and intra-trade, which is beneficial for South Africa. It highlights the significant costs Africa incurs due to its heavy reliance on external markets, emphasising the need to enhance resilience through stronger intra-African trade. The AfCFTA is expected to create opportunities for businesses to access new markets for goods and services, while also reducing the costs and bureaucracy associated with exports. South Africa stands to gain by venturing into new industries within the energy value chain, such as the beneficiation of minerals like manganese, cobalt, lithium, and copper for the production of battery technologies used in green energy. Enhanced trade and economic benefits can be anticipated through increased inter and intra-trade with other African countries, particularly within the SADC Economic Hub. The African continent remains a crucial market for South Africa’s exports, accounting for 24.4% of all merchandise exports and 40.2% of manufactured exports to the global market in 2022.

South African companies have the opportunity to participate in higher levels of intra-regional trade and investment activities. This includes expanding exports of consumer items, capital goods, and input materials linked to infrastructure development across the continent. Likewise, local companies can benefit from investment prospects associated with cross-border supply and value chain development.

Just Transition

The Just Transition project presents both opportunities and challenges for South Africa. On the one hand, there are risks associated with energy supply as coal-fired power stations are decommissioned. On the other hand, failure to embrace decarbonisation and green energy imperatives may result in the loss of funding for the development of new green energy power stations. South Africa, like many other African countries, has the potential to benefit significantly from the growing global green and digital economies. This can bring in new investment activities, including foreign direct investment (FDI), and create opportunities for export trade development. South Africa’s abundant mineral resources, such as copper, cobalt, platinum, nickel, alumina, and rare-earth minerals, among others, contribute to its potential in these sectors. However, the risks associated with the transition may have negative effects on the South African economy in the medium to long term.

State-Owned Enterprises (SOEs)

State-owned entities such as Eskom, Transnet, Denel, and the South African Post Office are still plagued by dysfunction. These state enterprises are in a state of disrepair, and their restructuring plans have proven unsuccessful. The oversight of SOEs lacks independence, with very few effective oversight mechanisms in place. Political influence hampers the ability of oversight mechanisms to guide SOEs in fulfilling their mandates. The setting of performance indicators and measuring the performance of SOEs by the relevant line ministry is often unclear, uncoordinated, and vague. Many SOEs struggle due to inadequate governance frameworks and the challenge of balancing commercial, developmental, and shareholder objectives imposed on them.

- Reduced capital inflows and foreign trade

- Decreased foreign direct investment (FDI)

- Depletion of external reserves

- Price increases on international market financing

- Decreased competitiveness in the global economy.

- Increased due diligence requirements for global trading.

However, the impact of grey-listing on a country can vary, leading to either negative or neutral effects. It is possible for a country’s standing to be restored if decisive actions are taken to address the concerns raised by FATF. The South African government is aware of these implications, and the finance minister has indicated that necessary measures, including regulations and action steps, will be implemented to address the outstanding deficiencies. This proactive approach is considered a positive step towards resolving the concerns raised by FATF.

RATING SENSITIVITIES

There are several factors that, either individually or collectively, could result in a negative rating review. These include:

- Inadequate assurance and ineffective management of the energy supply

- A weak economic growth outlook coupled with rising interest rates.

- High levels of consumer inflation

- Unsustainable increases in public debt

- Inability to address the economic sabotage of infrastructure.

- Weaknesses in Environmental, Social, and Governance (ESG) fundamentals

- Geo-political factors

These factors, if not adequately addressed, have the potential to impact the country’s credit rating negatively. The relevant stakeholders need to focus on mitigating these risks and implementing measures to strengthen the overall economic and governance landscape.

CONCLUSION

While there are rating pressures due to economic and social factors, the country’s resilience, proactive policy measures, and potential investment opportunities in infrastructure development provide a positive outlook. The government’s efforts to address fiscal pressures, enhance revenue generation, and promote economic growth are crucial for maintaining stability and improving the country’s creditworthiness. Continued implementation of structural reforms, effective management of public finances, and addressing socio-economic challenges will be instrumental in strengthening South Africa’s credit position in the long term.

Rating Methodology

Website link: Sovereign Rating Methodology: Governments/Sovereign States Rating History

Rating history