Booming energy industry, for the wrong reasons

Not too many ways to view load shedding (electricity curtailment) in a positive light but there are some interesting, potentially positive, side effects. Unintended consequences, like booming industries to compensate for what the state cannot provide. Booming business, but for the wrong reasons, though all much greener though.

Let’s be clear; booming industry and it being green is great and welcome, but being forced into the expenditure is toxic. And exclusionary not inclusionary at the same time. Not all can afford back-up or solar installations. What happens to the ones who cannot afford to finance the significant investment? Yes, they get left behind. So, remind me again how is this good for all? It is good. Just not for all.

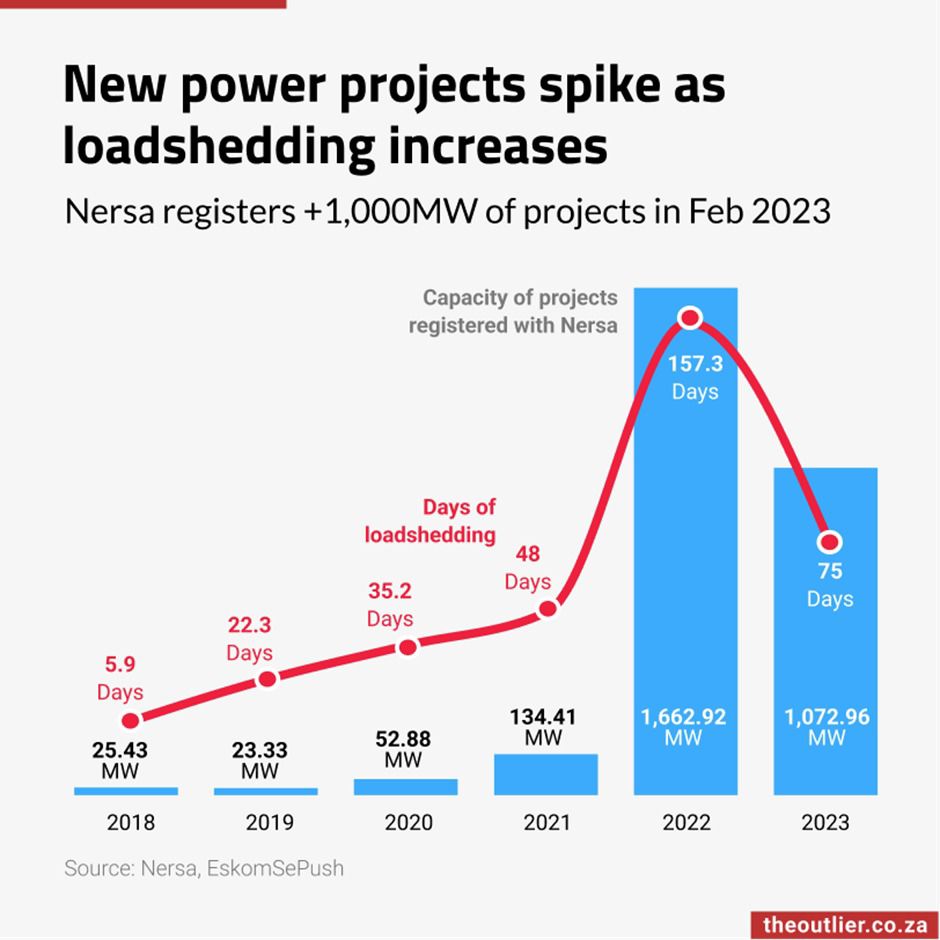

Load shedding sparked an unprecedented boom in the solar, battery and inverter installation industry. What used to be a niche market is now solidly mainstream. Installations are going through the roof. On the business, farming and mining side, new power generation projects using mostly solar and wind have seen a massive increase in the past 12 months.

According to NERSA, which registers power generation projects, the capacity of projects registered last month (1,073MW) was already nearly as much as the total capacity registered during the whole of 2022 (1,662MW), which itself was more than 10 times the capacity of projects registered in 2021.

After four years of steady increases in load shedding between 2018 and 2021 it seems, most businesses have started to embrace the inevitability of load shedding and started to invest in their own power sources.

The interesting potential side-effect of this is that in a few years, many SA businesses may well have a competitive, or even lower, carbon footprint than their international peers. Good for business and something not possible under SA’s primarily coal-powered state energy system.

***

Global Trade

After nearly five years of open economic conflict, the US-China trade relationship is beginning to show a “general pattern” of decoupling even as globalisation more broadly remains resilient, according to DHL’s global connectedness index.

US-China trade flows hit an all-time record in 2022 and yes, and the two nations are connected by larger trade flows than any other pair of countries without a common border. One of the main takeaways is that globalisation is not in retreat.

Still, the analysis dug deeper into the data and found that both the US and China have meaningfully reduced the share of their imports coming from each other and is indicative of economic decoupling.

Tariffs initiated by Trump in 2018 and maintained by President Joe Biden are the primary cause for the decline in US-China trade flows, according to the analysis.

US imports of Chinese goods that were subjected to the highest US tariffs, were 22% lower in mid-2022 than they were before the start of the trade war in 2018, while imports from the rest of the world were up 34%. In contrast, US imports of Chinese goods that were not subject to US tariffs during the trade war were up 50%.

The data make clear that international flows have proven remarkably resilient through recent crises, and they strongly rebut the notion that globalisation has given way to deglobalisation.

Today’s threats to globalisation, nonetheless, are real and demand serious attention. It would be a mistake to infer from the recent resilience of international flows that globalisation cannot go into reverse.

The report analysed various other data points too, including foreign direct investment, migration trends and scientific research collaboration, and found that the share of nearly all of these cross-border flows involving China declined since 2016.

Interestingly, they found little evidence that America’s allies were meaningfully decoupling from China and its allies in terms of merchandise trade.

While there were some declines in cross-border flows between US allies and China (and vice versa) the magnitude of the shift was much more limited than the decoupling observed between the US and China.

Even as US-China decoupling has advanced, it has not — at least yet — led to substantial fragmentation between rival blocs of countries.

Ten key takeaways from the report are shared below.

***

Ghana’s debt crisis affecting South African companies

South Africa’s four biggest banks (four of the continent’s five largest) plan to write off as much as $270 million of their investments in the West African nation’s bonds.

That equates to a haircut of almost 60% in some cases.

Firms in Nigeria and elsewhere will also have to take losses as the Ghanaian government works to restructure about $30 billion of its public debt. The costs to local lenders will only be known later.

They are just some of the losers from Ghana’s debt meltdown.

S&P Global Ratings forecasts haircuts on foreign securities of as much as 50%.

The nation isn’t alone in Africa in facing a debt crunch — Zambia and Ethiopia are also in talks to revamp obligations.

But the gold and oil producer’s fall from grace from one of the continent’s top investment destinations came as a shock.

Maybe it shouldn’t have.

Yes, COVID-19 and the impact of Russia’s invasion of Ukraine hit the economy hard, but a controversial (and now stalled) plan to build a cathedral in central Accra at an escalating cost of $400 million is a stark example of spending excess.

Ghana got itself into the bind, frankly, through poor financial management, and they’ve made political choices that give rise to these fiscal challenges. President Nana Akufo-Addo has defended his government, giving a list of projects in a speech to the nation that his administration has developed.

Investors did not expect that they would foot part of the bill.

****

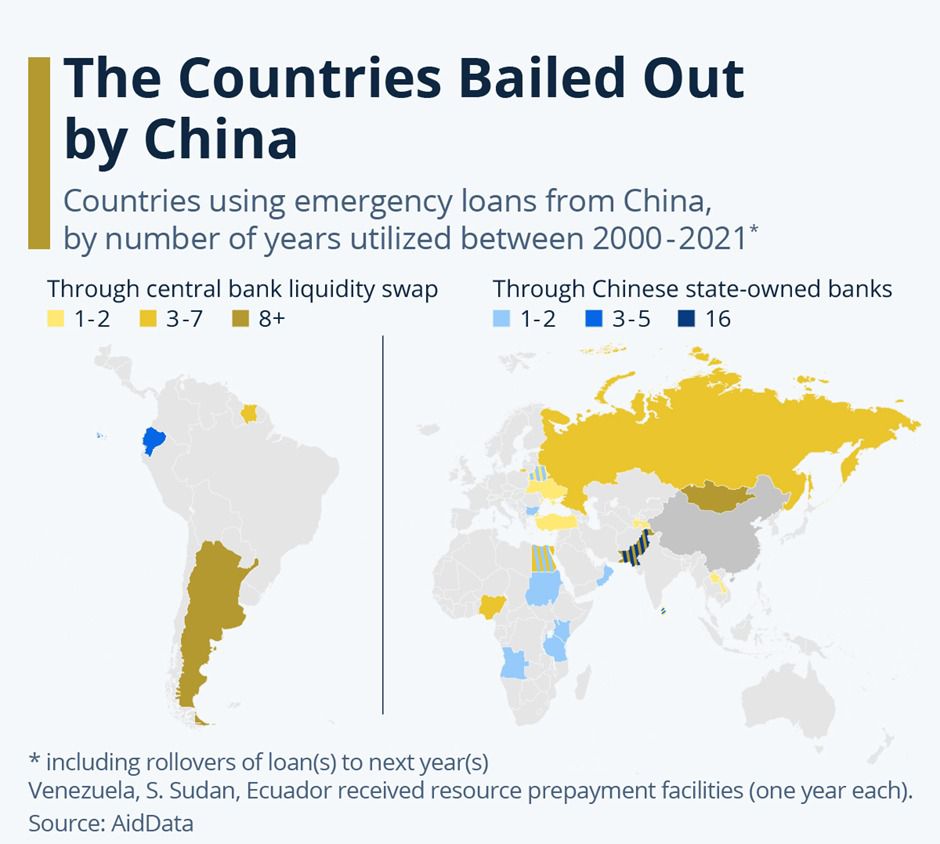

Countries Bailed Out by China

A new report published by the AidData research lab sheds some light on the usually non-transparent practice of Chinese bilateral emergency loans.

They identified 22 countries that were bailed out by Chinese loans when they ran into liquidity problems between 2000 and 2021.

Countries that utilised these loans in an especially high number of years, i.e., rolled over their loans into subsequent years include Pakistan, Mongolia, Argentina and Sri Lanka.

The latter tapped China’s central bank for the first time in 2021 before defaulting on its debt in 2022.

Argentina and Mongolia were also identified by the report as countries that have been in dire financial distress since the early 2010s and were using China as a lender of last resort despite the country’s loan terms being less favourable than lower-interest bailouts offered by the IMF or the US Fed.

The list of Chinese bailouts also includes countries experiencing major inflation events, like aforementioned Pakistan, Turkey and Egypt.

Bailout amounts provided by China remained quite low in the 2000s and early 2010s, before shooting up from 2015 onwards, climbing to a total of $100 billion for the two decades.

Source: Statista

****

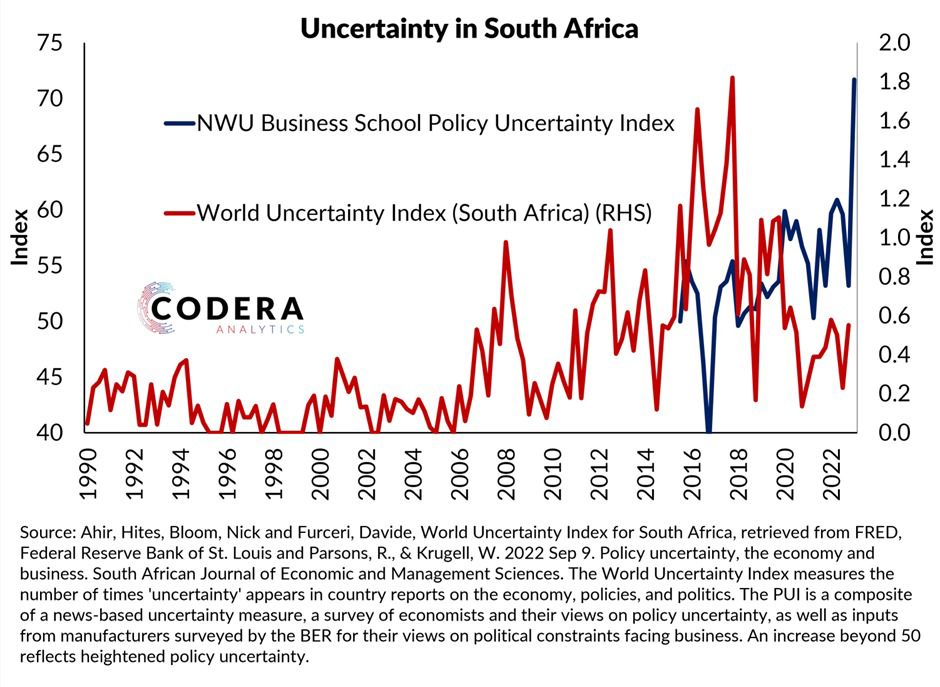

The latest Policy Uncertainty Index (PUI) from the NWU Business School spiked to a record level in 2023Q1.

Contributing factors include South Africa’s grey listing and worsening load-shedding.

The latest value of the World Uncertainty Index for South Africa is down from its 2017 highs, though it is published with a longer lag than the PUI.

Among the fundamental structural reform items is policy uncertainty.

Simple but fundamental to the investor community.

“Remember one cannot force people to invest, but you can create an environment which makes it easier to invest, create jobs and, hey presto, develop the country”… former Finance Minister Tito Mboweni, Feb 2021.