Jambo Africa Online’s Senior Editorial Correspondent, FRANCOIS FOUCHE, gives us a collage of news tit-bits from various sources that impact on Africa’s and global economies.

How to attract private finance to Africa’s development?

African economies are at a pivotal juncture. The COVID-19 pandemic has brought economic activity to a standstill. Africa’s hard-won economic gains of the last two decades, critical in improving living standards, could be reversed.

High public debt levels and the uncertain outlook for international aid limit the scope for growth through large public investment programs. The private sector will have to play more of a role in economic development if countries are to enjoy a strong recovery and avoid economic stagnation. Heads of state from Africa made this one of their resounding messages during the recent summit on “Financing African Economies” held in Paris in May.

Infrastructure — both physical (roads, electricity) and social (health, education) — is one area where the private sector could be more involved. Africa’s infrastructure development needs are huge — in the order of 20% of GDP on average by the end of the decade. How can this be financed? All else equal, the main source of financing would be more tax revenue collections, something that most countries are working towards. But, given the scale of the needs, new financing sources will have to be mobilised from the international community and the private sector.

Africa is a continent that holds immense opportunity for private investors. It has a young and growing population and abundant natural resources. Cities are seeing massive growth. Many countries have launched long-term industrialisation and digitalisation initiatives. But significant investment and innovation are necessary to unlock the region’s full potential. Recent research published by IMF staff shows that the private sector could, by the end of the decade, bring additional annual financing equivalent to 3% of sub-Saharan Africa’s GDP for physical and social infrastructure. This represents about $50 billion per year (using 2020 GDP) and almost a quarter of the average private investment ratio in the region (currently 13% of GDP).

What constrains private finance now?

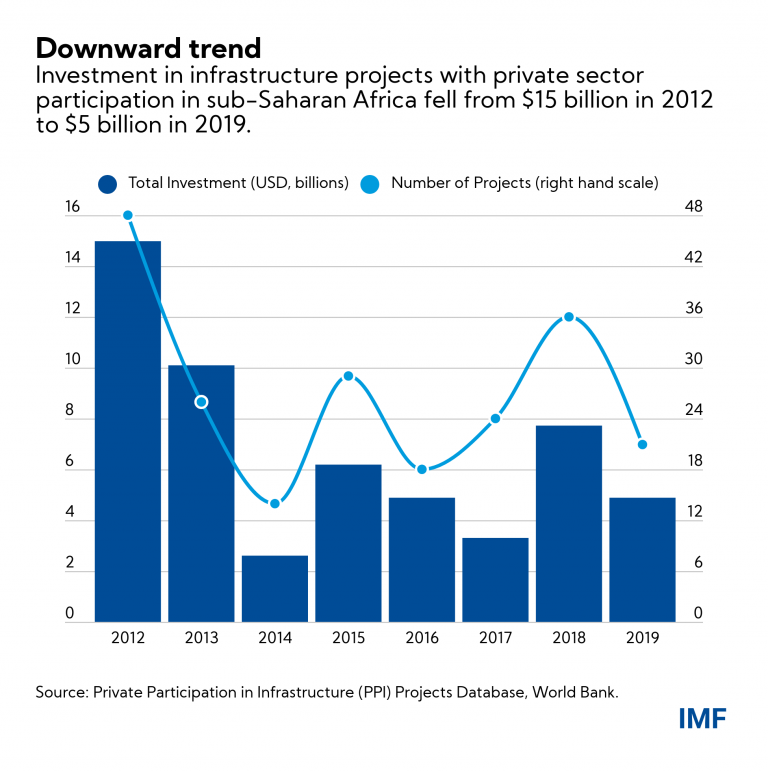

At the moment, the private sector is not involved much in financing and delivering infrastructure in Africa, compared to other regions. Public entities, such as national governments and state-owned enterprises, carry out 95% of infrastructure projects. The volume of infrastructure projects with private sector participation has significantly declined in the past decade, following the commodity price bust. The limited role of private investors is also apparent from an international comparison perspective: Africa attracts only 2% of global flows of foreign direct investment. And when investment does go to Africa, it is predominantly to natural resources and extractive industries, not health, roads, or water.

To attract private investors and transform the way Africa finances its development, improvements in the business environment seem critical. Recent IMF research shows that three key risks dominate international investors’ minds:

- Project risk. Despite Africa presenting a wealth of business opportunities, the pipeline of projects that are truly “investment-ready” remains limited. These are projects sufficiently developed to appeal to investors that do not want to invest in early-stage concepts or unfamiliar markets. Financial and technical support by donors and development banks can help countries fund feasibility studies, project design and other preparatory activities that expand the pool of bankable projects.

- Currency risk. Imagine that a project yields a return of 10% a year, but the currency depreciates by 5% at the same time — this would eliminate half of the profits for foreign investors. No wonder currency risk is a top concern for them. Prudent macroeconomic policy combined with sound foreign exchange reserve management can greatly reduce currency volatility.

- Exit risk. No investor will enter a country if they don’t have assurances that they can also exit by selling their stakes in a project and recouping their gains. Narrow and underdeveloped financial markets may prevent investors from exiting by issuing shares. Capital controls can slow down or increase the cost of exiting. And, when the legal framework is weak, investors may get bogged down in legal battles to have their rights recognised.

Incentivising private investment

Improving the business climate is important but not enough. Development sectors have certain structural features that make private sector participation intrinsically complicated, even in the most favourable environments. For instance, infrastructure projects often have large upfront costs, but their returns accrue over long periods of time, which can be difficult for private investors to assess. Private sector growth also thrives on networks and value chains, which may not yet exist in new markets.

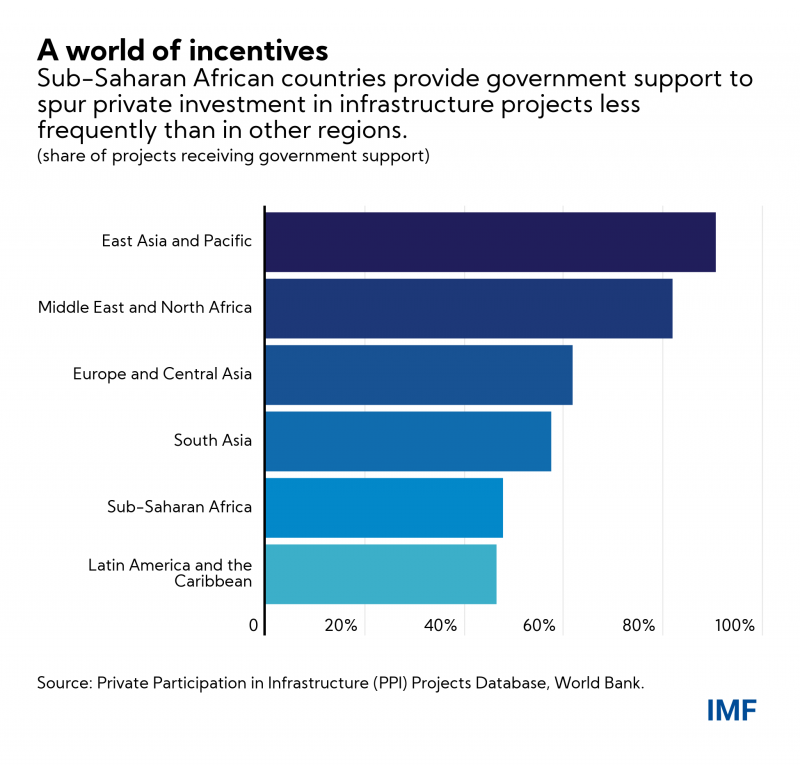

When these problems are acute, governments may have to provide extra incentives to make infrastructure projects attractive to private investors. These incentives, which comprise various types of subsidies and guarantees, can be costly and carry fiscal risks. But the truth is, many projects in development sectors won’t happen without them. In East Asia, 90% of infrastructure projects with private participation receive government support.

With certain design features, governments can maximise the efficiency and impact of public incentives, while minimising risks. Support should be targeted, temporary, and granted on the basis of proven market dysfunctions. It should also be transparent, leave sufficient risk to private parties, and display additionality, meaning that incentives should make worthy projects happen that would not happen otherwise. Finally, their size should be well calibrated to avoid overcompensating the private sector.

Given the limited availability of public funds, African countries and development partners could consider reallocating some resources used for public investment towards financing public incentives for private projects. When this reallocation is gradual and supported by sound institutions, transparency and governance, it could increase the amount, range, and quality of services for people in Africa. More innovative thinking can help realise the transformative potential of infrastructure on the continent.

This article first appeared here:

****

Progressive Africa

As the world turns away from oil, Gabon is exploring a novel way to replace the revenue that accounts for more than half of its fiscal budget.

The country has granted the African Conservation Development Group the right to sustainably develop a swathe of 700,000 hectares of land. The company plans to partially finance the project through bonds paid for by carbon credits earned from preserving its section of the vast Congo Basin rainforest.

In return for the concession, Gabon hopes to host an eco-tourism industry and sustainable hardwood logging operations, activities that generate considerable earnings in some other tropical countries.

It’s a gamble.

Carbon credits are not new, but in the past they’ve typically been generated from single projects, often to prevent deforestation. This is a plan to preserve a larger area with multiple land uses. Still, for a country with few assets other than oil, which is set to devalue in an increasingly climate-conscious world, it’s a gamble worth taking.

As the world’s second-most forested nation, Gabon has already had some success. It received $17 million this week under an earlier agreement for preserving forests.

If successful with its latest initiative, it could set a benchmark for other heavily forested countries in Africa, including the Republic of Congo and Cameroon. With a race to keep the earth’s climate from warming excessively, the world needs them. Forests across central Africa alone absorb 4% of the world’s annual emissions.

As Lee White, the English botanist who became Gabon’s environment minister, says: “If we lose the Congo Basin, we lose the fight against climate change. As a country we are trying to push the idea – rather than pay us for reducing emissions, pay us for absorbing emissions.”

Source: https://www.bloomberg.com

****

A clearer picture of the global economy’s health is starting emerge after months of difficult-to-interpret comparisons to a year ago.

South Korea posted an exports gain of almost 30% in the first 20 days of June from a year earlier, but the pace of rise was much slower than in May when they jumped by a 10-year high of more than 50%.

That’s because skewed base effects — in this case, comparisons to the sharp drops a year ago — are wearing off. International commerce underwent its roughest patch of the pandemic from March to May last year and started a painfully bumpy recovery last summer.

With summertime under way again (in the northern hemisphere) and low bases fading, South Korea’s export figures for all of June are unlikely to soar like they did in April and May but should still look healthy.

Underlying momentum remains positive with semiconductor manufacturers leading the charge, the export sector is poised to remain a key driver behind the rebound in South Korean growth this year — and likely into next.

The slower-than-earlier gains may sound disappointing to those who’d prefer to see a sharper V-shaped rebound, but it also means the world economy may be entering a more normal and regular phase of recovery. That should make the future easier for to predict and volatility easier for markets to grapple with.

Normalcy is what central banks including the Bank of Korea (BOK) may also like to see more of.

The BOK is calling for “normalizing” its record low interest rate when it becomes obvious the economy is back on track. A 29% exports rise so far in June may be the right number that justifies its focus shifting from recovery to stability — it’s not too hot, it’s not too cold. But it’s certainly reassuring enough.

Source: https://www.bloomberg.com

****

Benefits of setting a lower limit on corporate tax

On June 5, 2021, Finance Ministers from the Group of Seven major industrialised nations committed to a global minimum corporate tax rate on multinationals of at least 15%. While there are a number of details yet to be hammered out in broader global discussions, this historic agreement heralds an important step forward on the road to international corporate tax reform.

It also highlights the role minimum taxes can play at the global level to help reverse nearly four decades of falling global corporate tax rates and reduce the incentives for large multinational firms to shift profits to low-tax jurisdictions to reduce their worldwide tax liability.

A new IMF study examines how different types of domestic minimum tax regimes can help countries preserve their corporate tax base and mobilize revenue.

Minimum taxation over the decades

There is an unusual tension in the world of corporate taxation. On the one hand, countries compete vigorously to lure businesses and investors within their borders by offering numerous profit- and cost-based tax incentives, driving their tax rates down. On the other hand, governments decry these multinational enterprises—once they have been successfully attracted to the country—for not paying their fair share of corporate taxes, leaving the burden to fall on often-struggling local firms.

The bare minimum

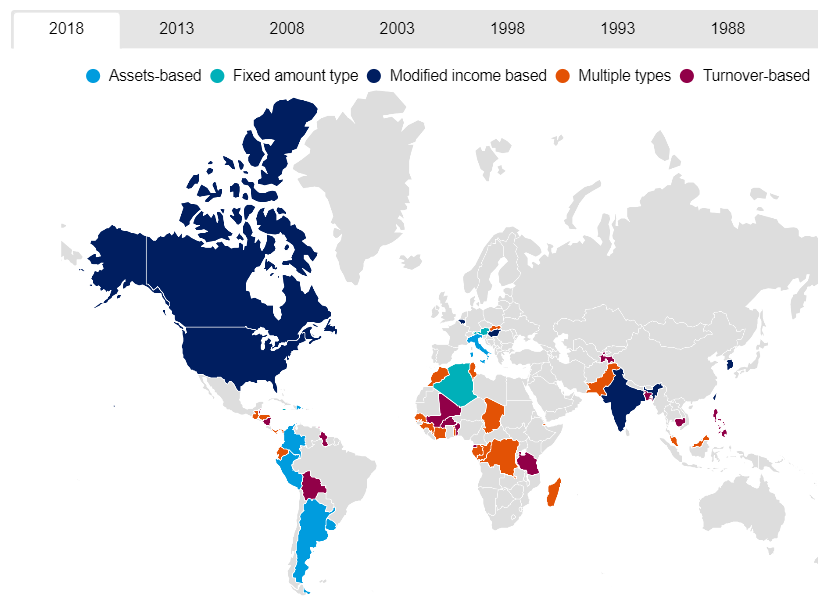

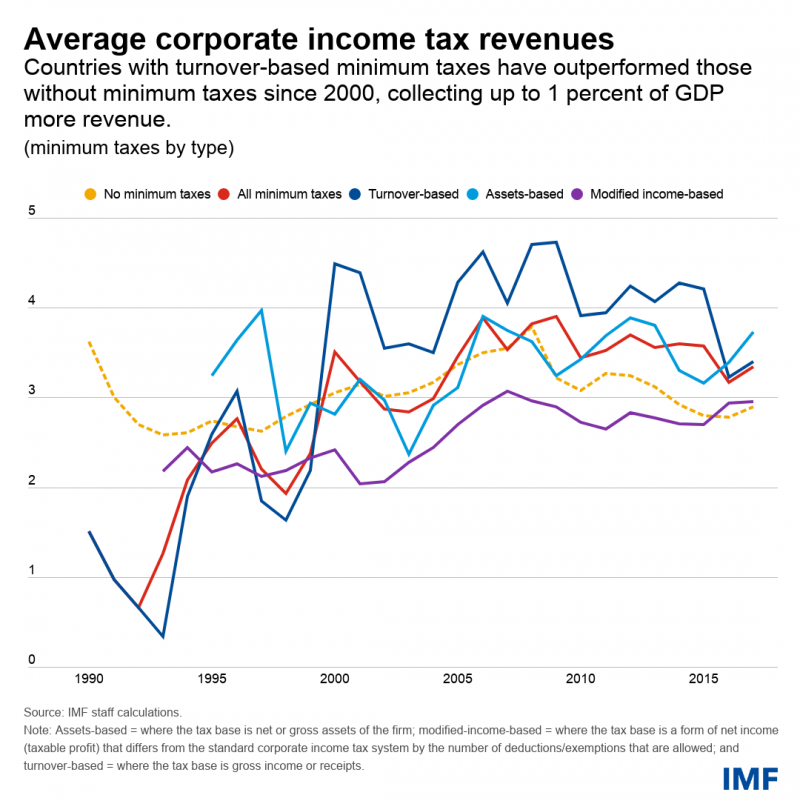

The number of countries with minimum corporate taxes continues to grow. In 2018, 52 countries levied some type of minimum tax.

(minimum taxes by type and country)

Source: IMF staff calculations.

Note: Country borders or names do not necessarily reflect the IMF’s official position. Assets-based = the tax base is net or gross assets of the firm; fixed amount type = minimum tax is a flat tax largely independent of the firm’s turnover, assets, or net income; modified-income-based = the tax base is a form of net income (taxable profit) that differs from the standard corporate income tax system by the number of deductions/exemptions that are allowed; multiple types = the country has had more than one type of minimum tax in effect over the sample period; and turnover-based = the tax base is gross income or receipts.

“The agreement reached by the G7 countries on minimum taxes has provided fresh momentum to the overhaul of international tax rules.”

Increasingly, governments are turning to minimum taxes as a means of preserving their tax base.

This is particularly true in developing countries with weaker tax administrations, which face major challenges in effectively taxing these large multinationals.

The idea of a minimum tax rate is not new. At the local level countries have been using modern forms of minimum taxation since at least the 1960s, taxing businesses on income generated based on activity undertaken within their territory. The goal of this “local” (domestic) minimum taxation is to prevent erosion of the tax base from the excessive use of what is known as “tax preferences.” These tax preferences take the form of credits, deductions, special exemptions, and allowances and usually result in a reduction in the amount of tax a corporation owes. By instituting a corporate minimum tax rate, governments guarantee a floor on the businesses’ contribution to the public purse.

Minimum taxes are typically computed using an alternative simplified tax base that avoids the complexities of the standard corporate tax base. They are often based on turnover (gross income or receipts) or assets (net or gross). A third alternative uses modified definitions for corporate income that explicitly limit the number of deductions and exemptions allowed.

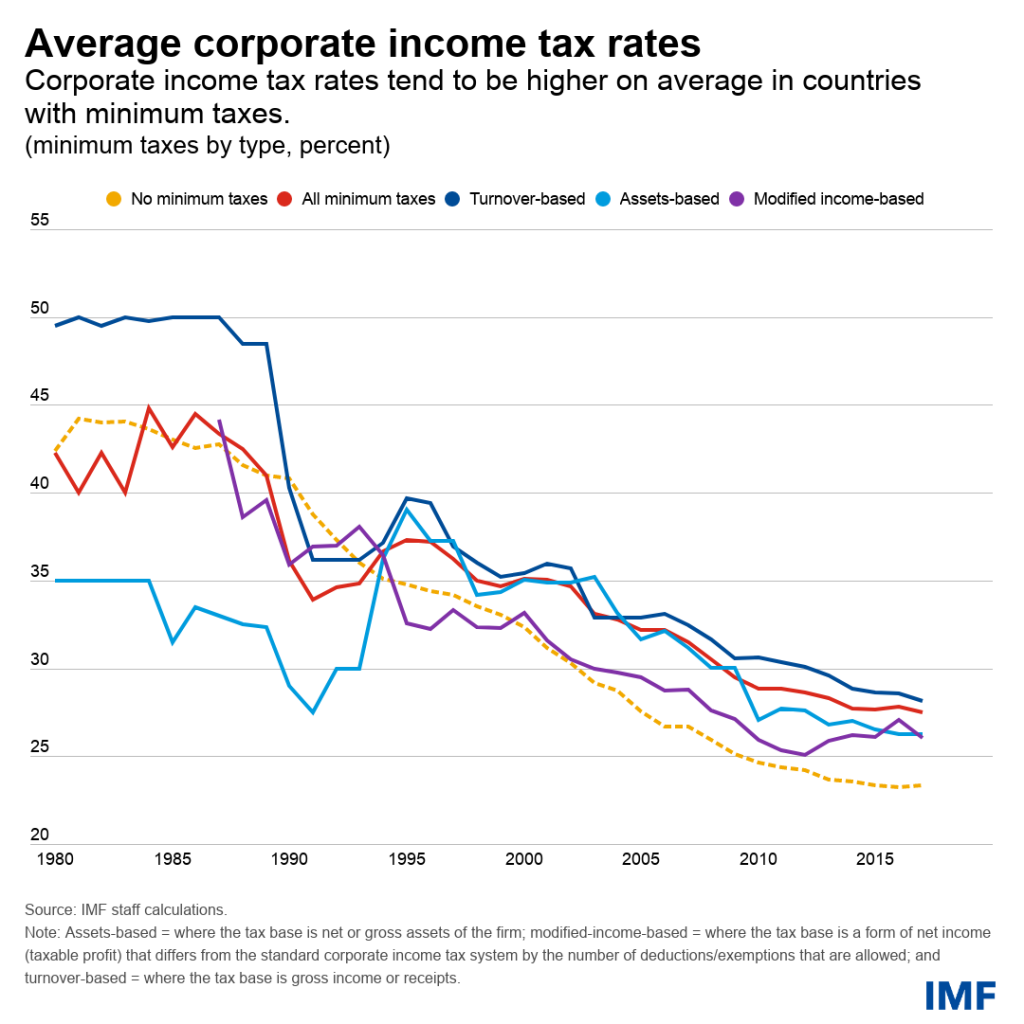

Using a new database of minimum corporate tax regimes worldwide, the IMF shows how minimum taxes have grown in popularity over the past few decades. Turnover-based minimum taxes are the most prevalent and tend to be found in countries with higher statutory corporate tax rates (the rate imposed by law). Countries that levy a minimum tax also tend to report higher corporate tax revenue as a share of GDP.

The IMF study the impact of minimum taxes on revenue and economic activity by combining their new country panel database with firm-level data. What they found is that introducing a minimum tax is associated with an increase in the average effective tax rate—that is, the tax rate actually paid by corporations after taking into account tax breaks—of just over 1.5% with respect to turnover and around 10% with respect to profits.

Minimum taxes based on modified corporate income lead to the largest increases in effective tax rates, followed by those based on assets and turnover. Ultimately, the revenue impact also depends on the rate applied.

In addition, the IMF used firm-level data to get a sense of the potential revenue that would result from the introduction of a hypothetical minimum tax of 0.5% on turnover and minimum tax of 1% on total assets. For the median country, the former could raise an additional 7% of tax revenue for governments relative to current levels and the latter almost a third more.

This translates into an average of 0.2 and 0.9% of GDP in additional revenue—for the median country in their sample—for a turnover-based and an assets-based minimum tax, respectively, on top of a median corporate income tax-to-GDP ratio of 2.7% These results represent a significant revenue potential that merits serious policy consideration.

Fresh momentum

The agreement reached by the G7 countries on minimum taxes has provided fresh momentum to the overhaul of international tax rules led by international organizations. As part of this overhaul, the Organisation for Economic Cooperation and Development (OECD) and the G20 had proposed in late 2020 a global minimum corporate tax that would apply to profits of multinationals. Countries would still set their own local tax rates, but if a multinational company paid less than the global minimum rate in another country, that company’s home or source jurisdiction could supplement its tax liability to ensure it paid the minimum. In this way, the advantages of shifting profits to low-tax jurisdictions would be reduced.

The OECD and G20’s global proposal differs from standard local minimum taxes—it would not focus solely on income generated on activities undertaken within a country. Instead, payments would be triggered only if other countries don’t tax multinationals enough. Furthermore, the use of local minimum taxes could end up increasing as they provide a simpler alternative to the complex provisions of this proposal for a global minimum tax, which many low-income and developing countries may not have the capacity to implement.

Powerful but not perfect

Despite inefficiencies associated with local minimum taxes, they could allow countries to tap significant revenue. In this way, setting a floor on corporate taxation—at least at the local domestic level with moderate tax rates—can be a good option for countries looking to preserve revenue and prevent the erosion of their tax base without severely damaging corporate activity.

However, minimum taxes alone cannot replace reforms that broaden the corporate tax base. The proliferation of multiple rates and all sorts of special preferences within the standard corporate tax system causes costly distortions and low revenues—and encourages tax avoidance and evasion. Tax incentives to attract multinationals are also likely to persist even after the introduction of a global minimum tax, as countries will continue to do what they can to entice foreign investment for growth and development. But the value of these incentives will decline, as multinationals will only be able to reduce their liabilities to 155 and not zero. And so, therefore, the first best remains to tackle and remove these head on.

This article first appeared here: